- Do it yourself that is an intelligent tip because best sort of renovations increases the value of the house and simultaneously raise the amount of security you have got.

- Debt consolidation reduction if you have current expenses elsewhere, you might release domestic guarantee and rehearse the money to blow men and women bills out-of. Not simply are you willing to mix the money you owe together, but you can along with capitalise on all the way down rates of interest of household collateral financing and you can reduce the payment. There are other methods of debt consolidating we touch on by the end of guide.

- High commands they are always pay money for huge-pass things such as vehicles, costly vacations if not college or university degree.

- Enabling members of the family people choose to use these to availableness borrowing and provide it so you can family relations to assist them log in to the house or property ladder and other setting. The financial institution out-of mum and you can dad try real!

You can find rarely one limits put on what you are able invest the money for the. So long as you prove to the lending company that you can afford the payment per month and you’ve got a great credit rating, that’s it that matters on it.

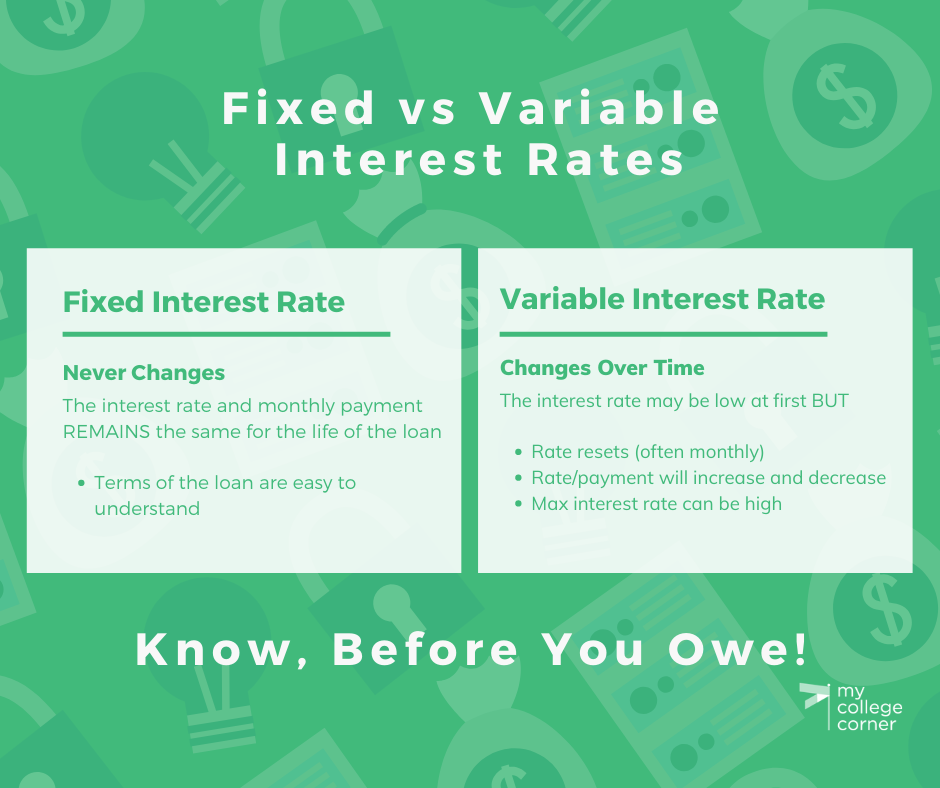

The speed into household equity funds

Among the many aspects of a home security loan a large number of some one such as for instance are the interest rate. Not only could be the interest levels in these financing less than really signature loans, they generally have repaired month-to-month desire. That have a fixed interest, you’ll be able to always know exactly how much your payment per month was along the entire mortgage payment several months.

What is a property security personal line of credit (HELOC)?

A home collateral personal line of credit (HELOC) is like property collateral mortgage which includes key differences. A house collateral line of credit lets this new resident to gain access to borrowing from the bank in line with the guarantee he’s got within their property that have their home since the security, although cash is maybe not paid in the a lump sum.

Rather, the financing is actually accessed over time on homeowner’s discretion more a draw period, that history many years. An effective HELOC try an effective rotating credit line and you may work into the indicates like credit cards, opening an amount borrowed when necessary. Only if the brand new draw period closes do the citizen begin making a monthly payment to blow back the loan amount in full, for instance the prominent and you will notice.

The pace to the a good HELOC

Some other secret difference between property security mortgage and you can house security credit lines ‘s the interest rate. internet Whereas the former is frequently fixed, a house collateral personal line of credit typically has a changeable rates. You are able to spend adjustable notice along the entire repayment months, meaning your payment can move up and down and you may not 100% certain of exactly what you’ll are obligated to pay.

What is the newest interest into property guarantee financing?

The current interest levels into household guarantee funds are very different anywhere between loan providers and will also be based on your loan so you’re able to worth proportion, personal earnings and you may credit history. Although not, in accordance with the current market during composing, you can constantly get a hold of domestic equity finance with an interest rates anywhere between dos% and you will 9.9%.

Costs are usually all the way down if the installment loan label is shortened. Such, when you need to pay back more 5 years you may be able to get a diminished rate than just for folks who wanted to pay more fifteen years.

The average interest rate for the house collateral loans

The average interest getting a home equity mortgage within lifetime of creating and you may susceptible to alter is anywhere between 5% and 6%. If the mortgage name is actually quicker, the attention drops from the budget anywhere between these types of figures and vice versa.